By Daniel Margrain

For many people, buying a property is the biggest long-term investment they will make in their lives. The problem, however, is that the systemic frailities of the current financial system means that the ‘nest egg’ is not all it seems on the surface.

When banks lend money to people for a ‘mortgage’ – literally translated as ‘death grip’ – the increasing circulation of debt-fueled cash results in greater demand for property when supply is low. This has a knock-on effect in terms of rising prices.

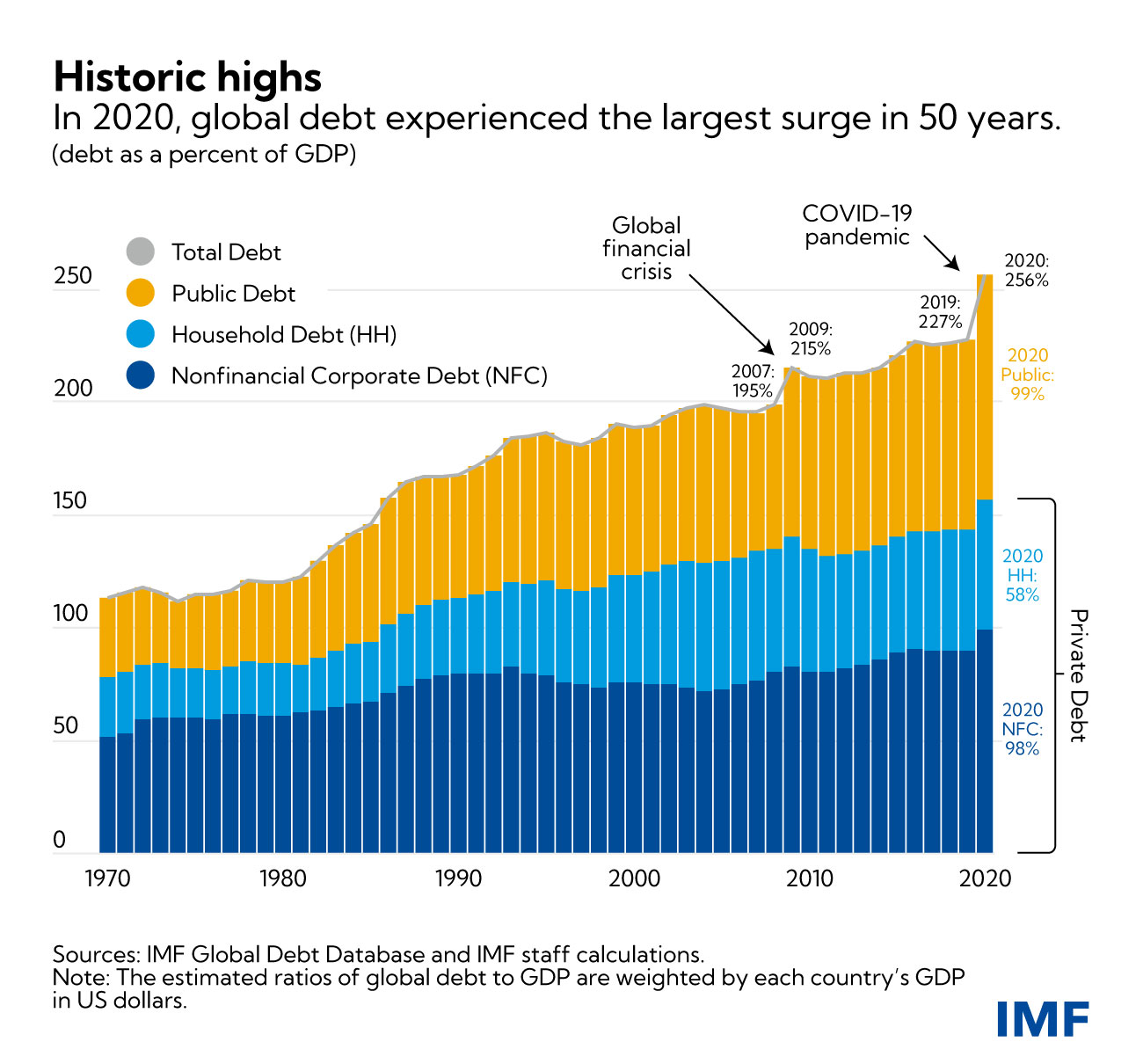

For the bankers, this process amounts to an apparent never ending cycle of growth. But for society in general this means an increasing mortgage debt burden which has culminated in global record levels of overall debt. According to the latest update of the IMF’s Global Debt Database, global debt rose by 28 percentage points to 256 percent of GDP.

Private debt from non-financial corporations and households also reached new highs. Increasing demand has exacerbated expanding household debt levels which, in the case of the UK, for example, is already tipping 65 thousand pounds per household.

The accumulation of public debt now accounts for almost 40 percent of total global debt, the highest share since the mid-1960s. Since 2007, this accumulation of public debt is largely attributable to the current global financial crisis.

The political response to the Covid pandemic and the Russia-Ukraine conflict has exacerbated a crisis that largely resulted from the fact that people continue to buy houses and goods with money they don’t have. In the UK, we can see how this insane system has played out in terms of the relationship between house price and stock market inflation and what we have been told has been a growth in living standards.

The price of nearly all assets – shares, bonds, property, land etc – have been on an upward trajectory for the best part of fifteen years since the last crash. And yet the economy is no better then it was in 2009. “Green shoots” have been talked about ever since but never materialized.

This is because stock markets, and particularly house prices, have no bearing on reality. This false reality is sustained because bankers motivated by short-term gain, have persuaded people to buy assets. If, for instance, a large swath of people invest their money into the same company by buying shares, then the value of those shares will increase and so will their return on their initial investment.

The current record level of debt is predicated on historically low levels of interest. The problem is as interest rates are now beginning to climb, it is putting more people into debt which has a negative knock on effect in terms of housing demand.

This has a downward pressure on prices. For those people who took out variable mortgages at the peak of the bubble, any increase in mortgage rates mean they are likely to fall into a negative equity. The FT reports: ”A pandemic-induced property boom peaked at the end of 2021 but the sector is now braced for the broadest slowdown since the financial crash.” Under these circumstances buying a house becomes less of an attractive option.

One might think that putting savings into a bank would be a more secure alternative than taking on a potentially precarious mortgage debt. But this isn’t necessarily the case. The Financial Services Compensation Scheme (FSCS) is supposedly intended to cover depositors for a limited amount invested per bank in the event of any collapse.

But under such circumstances, depositors’ would likely panic and demand all of their cash back at the same time. Inevitably, there would be shortfall of available cash since the banks wouldn’t be able to release it on mass given that it would almost certainly be tied up in high risk off shore investments.

Moreover, governments’ are not in a position to underwrite each individual depositor. Since the 2008 crisis, the official establishment line has been that governments’ would not allow banks to collapse because as institutions they were too big to fail.

The problem is that the reach of these banks is greater now than previously because other smaller banks that were teetering on the edge have been swallowed up by the larger ones. So the banks who in 2008 were regarded as being too big to fail are even bigger in 2023.

In the event on a run on banks, the priority of government is not to protect depositors, but rather, to protect the bankers from their own incompetence and proflicacy One of the main functions of the banking racket is to ensure the ‘socialization’ of losses and the ‘privatization’ of profits. So for them, it’s ‘win-win’ situation.

The close knit ‘revolving door’ culture that exists between retired parliamentarians’ taking their places on the boards of financial companies’ and the fact that irresponsible actions of bankers continue to be underwritten by the tax payer, means there is no incentive for either parliament or banks to change their destructive ways.

With property prices now in decline, against a backdrop of low growth, rising inflation and the Russia-Ukraine conflict coming on the back of the international response to the Covid crisis, it’s not unreasonable to assume that the property market will take a huge hit sooner rather than later.

The last time the real estate bubble burst, the global economy plunged into the deepest downturn since the Great Depression. The public, therefore, might be advised to increase their liquidity by ensuring they have access to physical money.

But there is another potential problem. The move towards Central Bank Digital Currencies implies the phasing-out of cash which will almost certainly mean increasing demand for precious metals like gold and silver.

As society and economy begins to ‘reset’ on a new footing that reflects a move away from the current Fiat system, a concomitant new paradigm with regards to the way human beings attribute value to their lives, is also likely to emerge in the post-interregnum new world order.